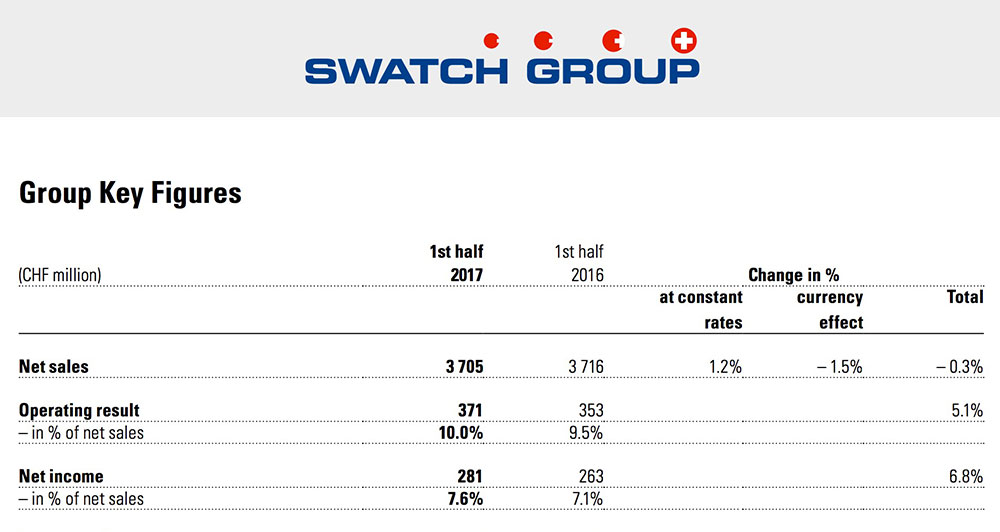

The Swatch Group has today released its half-year report. While we don’t need to cover every fluctuation of revenue and net sales at each major Swiss watch conglomerate, this provides a snapshot of where the group and the industry are at, and how its ongoing problems are being addressed. Yes, ongoing. While the Swatch Group report and others, such as that from the FH recently, want to suggest a sunny outlook, many underlying causes of the industry’s troubles remain. You can find the full report with all the specific data linked to below.

The Swatch Group’s report offers some interesting insight into the plans and activity of the world’s biggest group of Swiss watch brands. Such reports are specifically prepared for investors and market analysts – so the information tends to skew as favorably to the preparer as possible. With that said, things could indeed be worse. So let’s explore what the report says as well as what insight we can glean about current Swiss watch industry performance and where things are going.

In short, the Swatch Group has remained surprisingly sober, acting predictably but offering few insights as to its future plans. Swatch makes a few more or less unsubstantiated claims about future growth and performance potential, but that is standard in reports like this. Essentially, as bad as things are in the industry, they have commendably juggled their resources to hedge the potential problems they could have had.

The report shows that sales are down ever so slightly, but margins are up. How is that possible? Cost-cutting. The reason for the better margins is related to fat-trimming measures – mostly in personnel, as most other areas of spending are more or less stable. This is a very (very) sensitive area for a Swiss company because, in many Swiss people’s opinion, among the worst things you can do is terminate employees. You wouldn’t emphasize the desire to keep jobs unless you are trying to calm feelings to the contrary, but it is clear that personnel costs are down compared to the same time last year. The reality is that, like other groups, the Swatch Group has let go of a lot of people, but perhaps not as many as they “should” from a business perspective.

The Swatch Group did see increased operating revenue margins from lower personnel costs, but they make a point to mention (more than one time, I might add) that they are working hard not to terminate jobs, and to retain as many production workers as possible. That includes the many men and women who are involved in not only the assembly of watches, but also the production of the many parts that go into watches. Allow me to further point out that this includes parts meant to go into Swatch Group brand watches, as well as parts for watches sold to third-parties such as the movements made by Swatch Group-owned ETA.

Swatch offers some interesting reasoning for why retaining as much of the production staff as possible is a sound idea. They seem to feel that market demand will rebound in the near future, and the group will be in a materially compromised position if they do not have the available human resources to operate the factories that are intended to fulfill the demand. I would take this reasoning with a grain of salt – and while it does likely represent the group’s hopes, nothing in the report offers compelling evidence for a serious market rebound in the near future. Though it is interesting to see that according to the Swatch Group, Hong Kong has “stabilized” – meaning they are no longer seeing numbers in that region that are so important for the industry fall.

Swatch makes it clear that sales to third parties are down. Those are authorized dealers, though they claim that this is somewhat being helped by brand boutique sales. Basically, wholesale is down and there is a shift for vertical integration with sales. That is a big deal, and it shows movement toward genuinely addressing the systemic issues that have held the industry back for so long.

For a while now, I’ve been saying that until the watch industry sees market performance stabilize (i.e., plateau) they will not act or invest in growth strategies. This behavior is well-reflected in the current spending habits of the Swatch Group which appear to be maintaining stability of the organization and not investing in too many new projects as one might anticipate happening. Why spend during hard times? Because people simply have more time. When sales and production needs slow, management has the ability to refocus and revise teams, processes, and entire departments. This is known to be happening, but it also appears to be happening in an efficient manner without major new expenditures.

When discussing areas of potential revenue growth, it is interesting that the Swatch Group seems to almost randomly choose models from its various brands (aBlogtoWatch suggested more areas of possible watch industry growth here). They don’t seem to back these claims up with numbers or evidence, so it feels as though they are just name dropping their own products. I think they don’t really know what the next big thing will be – and that is OK.

Early in the year, the Swatch Group reported optimism for 2017 despite that overall income had declined by half in 2016, and the new numbers at least don’t contradict that. The real takeaway message here is that the group and the wider industry aren’t really doing anything dramatic. It feels as though they are waiting for “something” to happen before making material strategy shifts, but they will eventually need to do more. Find the Swatch Group 2017 half-year report here. swatchgroup.com